Factoring

Working capital optimisation along the whole of your supply chain

Factoring is an excellent complement to traditional bank financing and expands a company's financial flexibility. By selling outstanding receivables, companies can quickly and easily gain more liquidity. Factoring should be initiated during "good times" to provide security for more difficult times and crises. Receivables financing therefore represents a perfect and modern form of corporate financing and has the advantage that the financing lines can always be customized.

As part of Erste Group, Intermarket Bank is the leading specialist for factoring and supply chain finance (SCF) in Austria.

Factoring briefly explained

- Corporate customers sell existing and future receivables to Intermarket Bank, which pays an advance on them before maturity.

- Intermarket Bank pays out up to the agreed advance rate (usually 80 to 90%) of the invoice amount, with the remainder paid upon receipt of the invoice. Companies gain liquidity and can decide daily whether and how much advance they need.

- For corporate customers with annual revenues of approximately one million euros or more. There is no upper limit.

- Customers can protect their receivables against payment defaults through Intermarket Bank. We work with credit insurance partners for this purpose.

- Intermarket Bank also handles dunning for customers upon request.

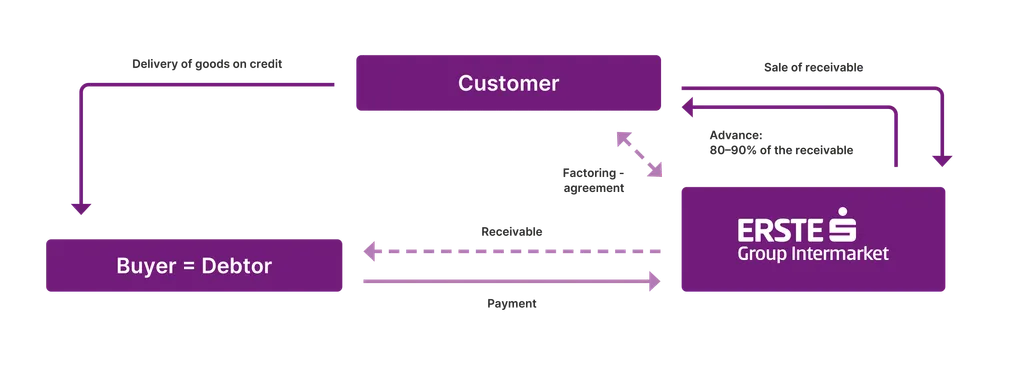

How factoring works

- The supplier delivers goods or services to the buyer and agrees on a payment term with the buyer.

- The supplier sells the receivables from this transaction to Intermarket Bank in the form of a factoring agreement.

- Intermarket Bank pays an advance of up to 90% of the gross invoice amount (including VAT) to the supplier on these claims.

- The buyer shall pay the invoice upon maturity to Intermarket Bank or to an account assigned to Intermarket Bank.

- After payment of the invoice, the supplier receives the remaining amount from Intermarket Bank (less financing costs).

Advantages

- Alternative liquidity protection

Factoring is based on the volume of a company's existing receivables for goods and services. This makes it independent of fixed credit limits and does not increase the factoring customer's bank exposure. - Broader financing base and greater financial flexibility

Factoring is a civil-law purchase of receivables; the risk is transferred to the large number of debtors. The receivables can be advanced immediately by the intermarket bank, giving the company greater flexibility in its daily liquidity and working capital management. - Greater security and risk protection for bad debts

By assuming the default risk with Intermarket Bank, the company protects itself against payment defaults on the debtor side. Upon customer request, Intermarket Bank will insure the receivables or refer the customer to a partner, such as Acredia Credit Insurance. - Balance sheet reduction and rating improvement

Optimized balance sheet structure through a higher equity ratio and improved financial strength. - Increased efficiency in accounts receivable management

Factoring leads to better discipline in accounts receivable management, improved data quality, and a reduction in overdue payments. Risk monitoring of the creditworthiness of buyers is also underway.

Target groups for factoring

Suitable companies

- Corporate customers with an annual turnover of 2 million euros or more, no upper limit

- Companies that deliver on open account with payment terms

- Companies with trade receivables from other companies (B2B) that can sell these to the factoring bank for financing without restrictions or bank collateral

- Expansive companies with dynamic sales growth and seasonal fluctuations

- Companies that want to improve their rating and focus on their working capital

- Existing start-ups with prospects for expansion

- Companies that want to open up new sales markets in foreign industries or foreign markets

Unsuitable companies

- Companies in the construction and related industries (construction companies, tilers, carpenters, electricians, floor fitters, etc.)

- Obvious restructuring cases without a going concern prognosis, whereby companies with a positive going concern prognosis or companies in insolvency can be supported

- Companies with a high proportion of private customers (in these cases, economic information is often not available or consumer protection and data protection regulations restrict the sale of receivables)

- Rent or commission claims (for factoring, the entrepreneurial service must be based on a delivery of goods or a clearly traceable service)

- Project business with advance payments and partial invoices over longer periods

- Payment terms of more than 180 days (exceptions with longer terms are possible, but usually not more than 360 days)

- One-off transactions or individual projects

- Companies with a high proportion of cash and card payments or a high proportion of private customers (retail)

Products

*) Recourse: Intermarket Bank may reclaim pre-financed amounts if the company's customers fail to meet their demands.

**) Non-recourse: The default risk is fully borne by Intermarket Bank.

Costs

The costs for factoring depend on:

- Amount of your annual turnover

- Use of dunning procedures and/or receivables insurance

- Creditworthiness and structure of your debtors as well as outstanding amounts

Factoring costs vary depending on the company. However, in every case, factoring ultimately yields more than it costs.

The total costs for factoring consist of the following sub-areas:

- Factoring fee – depending on the type and scope of the agreed service provided by Intermarket Bank

- Interest – for the advance payment of receivables

- Limit fee – for granting insurance limits within the framework of credit insurance

- Other fees – for example, the e-factoring fee or fees for payment transactions

Essentially, the costs can be compared to working capital financing.

Factoring is handled directly through Intermarket Bank. If you have any questions, please contact a customer service representative.

Intermarket Bank AG

Since 1971, Intermarket Bank AG has been a reliable partner in working capital financing along the entire value chain and is the specialist institution within Erste Group for supply chain finance.

As cross-company optimizations of financial structures and costs, supply chain finance solutions are becoming increasingly popular in today's business world. Tailor-made solutions for financing and risk hedging along its clients' supply chains are among Intermarket Bank's core competencies.

Embedded in or in cooperation with Erste Group, Intermarket Bank offers its customers innovative financing products and digital platform solutions in the areas of supplier financing (ErsteConfirming), inventory financing and factoring.

Since mid-2011, Intermarket Bank AG has been part of Erste Bank der österreichische Sparkassen AG. In January 2017, the shares of Erste Bank der österreichischen Sparkassen AG were transferred to Erste Group Bank AG. With this competent and strong background, we are one of the specialists in the domestic market when it comes to receivables financing. Especially in times of Basel III, free equity is a key component for the stability and growth of your company.