27.02.2018

International Women’s Day: Increased awareness on the topic of financial independence

- 8 out of 10 women want to be financially independent

- Increased awareness on the topic of financial independence

- Every second couple keeps separate accounts

- Controversial subject money: Fixed costs and contribution to household income point of contention

Almost half of the Austrians living in a relationship manage their finances jointly. They discuss financial matters and decide on them together (67 percent). Nevertheless, this harmony is deceiving because every other couple argues about money. One reason for that, especially for women, is the financial dependence on the partner. 6 out of 10 Austrian women said that in their relationship it is the man who is the main earner and that makes them dependent on the partner, financially speaking. 7 out of 10 of these women moreover said that they would not be able to maintain their current standard of living on their own. Another problem in this respect is that they neglect to make financial provisions for themselves, which would be very important, though.

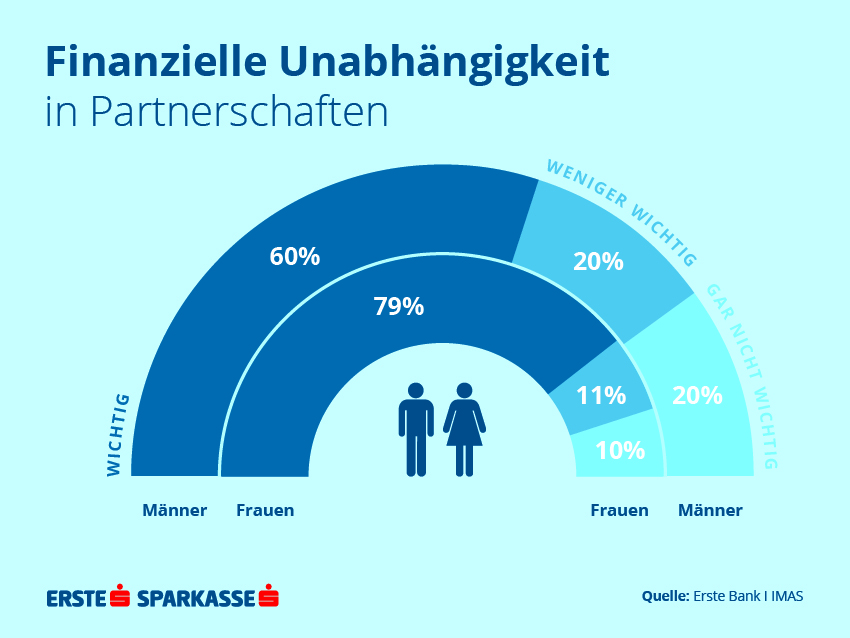

"In a relationship, everyone should have their own bank account and old-age provision. We can no longer rely on the state or the life partner to take up the slack," emphasizes Bianca Schwabl, investment expert at Erste Bank. And Austrian women are becoming more and more aware of this. As a representative study carried out by IMAS and commissioned by Erste Bank und Sparkassen shows, women who live in a partnership would like to be financially independent. To 8 out of 10 women, this independence is important in a relationship - compared to 4 out of 10 men. Especially separate accounts become more important to women who live in a partnership (+8%, 2018: 58%, 2017: 50%), while joint accounts are acceptable to an ever smaller number of women (2018: 18%, 2017: 23%). The fact that women save more for themselves makes it also clear that they want to stand on their own feet financially. This development is increasingly being noticed and even supported by men. About half of the men set money aside for the woman they are in a relationship with. Compared to the previous year, this figure increased by 6 percent (2018: 50%, 2017: 44%). „This development is positive. Nevertheless, women should not forget about their old-age provision. You might want to discuss this important topic with your bank adviser as he/she can inform you about different options," says Karin Kiedler, Head of Market Research at Erste Bank.

Already every second adult worried about money

50 percent of the Austrian men and women already worried about money some time in the past. Loss of income is stated as the main reason for this. It is striking that more women than men were affected by that (ratio: 42% to 36%). "Due to maternity leave and part-time work women experience disadvantages relative to income and that's exactly what brings us back to the misery of financial dependence," says Kiedler. Other troublemakers are high home loan rates (18%) or high unexpected costs (15%). But also ill health (14%) is cited as a reason. Kiedler: "Leisure-time accidents that are still underinsured may be an explanation for the latter. It is relatively easy, though, to make provisions for such a case by taking out an accident insurance. With regard to questions about money and financial matters, personal contact is important to Austrians. Their bank adviser is the number-one contact point for 78 percent of the Austrians, followed by the partner (52 percent), the family (46 percent), and friends (34 percent). Internet (31%) and media (23%) play a minor role. Every third couple sees the bank consultant together. In another third, one of the partners takes care of it for both and in another third, every partner keeps individual appointments with the bank consultant.

Controversial subject money: Fixed costs and contribution to household income point of contention

Especially when making financial decisions together, conflicts are inevitable for every second Austrian couple. Every fifth couple regularly argues about money, every third occasionally. Issues are primarily unevenly distributed fixed costs and the contribution to household income. Especially men complain about the latter (62%). However, this complaint is based upon the fact that as more women work part-time and take maternity-leaves, the man continues to be the principal earner in the relationship and he is aware of that. Another topic of discussion is when different priorities are set for expenditure, when money is constantly short or when money is carelessly spend. "The well-known handwritten budget book definitely had its justification. However, these days, more modern versions exist. In our digital banking app George, you can categorize all receipts and disbursement and get a very good overview of how much you spent on what," says Schwabl.

Women are less interested in securities than man

On average, women currently save 220 Euros per month, men 269 Euros. Since 2014, this amount has risen steadily with both sexes. The Top 4 reasons for saving money continue to be nest-egging (74%), financial security (70%), saving for larger purchases such as a house, a flat or a car (53%) and providing for the future (36%). When it comes to savings and investment products, both sexes favour security. Building loan contracts, savings accounts and life insurances are on the top of the popularity scale. Shares, funds or bonds are noticeably less interesting. The gender comparison shows clearly that women have different interests: while only 1 in 5 women (19%) is interested in securities for example, 1 in 3 men is (37%). Yet that this might be the wrong strategy as far as investments are concerned is illustrated by the following example: If you had paid 5,000 Euros into your savings account five years ago, you currently would have around 4,700 Euros. On the other hand, if you had opted for a fund with a 50 percent equity stake, you would have 5,600 Euros by now. "This example clearly shows that if you only focus on the passbook in times of low interest rates, you lose money. Securities are currently an important option, especially for retirement provision. With inflation at almost two percent and a key interest rate of zero, the loss of purchasing power is quite obvious," emphasizes Schwabl. Around three months' salaries should be available on the passbook for short-term expenditures. Planned investments should be hedged with products with mid-term investment horizons of approx. 5-8 years; long-term investment options should be selected for retirement provision. Schwabl emphasizes:"Build up your provision on three pillars, cover your financial needs with short-, medium- and long-term investment options. When it comes to old-age provision, the sooner you start, the better."

Money rain: What the Austrians wish for

What wishes would the Austrians fulfill themselves with a sudden cash injection? Travelling and purchasing real estate rank first and second with both sexes. When it comes to third place, however, the dreams of men and women differ: While a new car is very popular with men, women would like to share some of the money rain with their children and family members.

About the survey: On the occasion of International Women’s Day, Erste Bank hired market research institute IMAS to conduct a telephone survey on the subject of “Women and Finances”. From 23 January to 2 February 2018, 500 people were asked among other things about financial matters in their partnerships, money as a dispute factor in relationships, financial provision and who the consult in financial matters. The results are representative of the Austrian population aged 18 and over.

{kind=link}